Not being paranoid or anything but we were curious about the skills of the latest innovation to take the world by storm, ChatGPT, and its ability to work with the Australian tax system.

Let’s start by saying that we were impressed. Not so much by ChatGPT’s ability to work with the complexities of the tax system, but for its tone and approach. The outcome from our testing, including the example below, is that you might end up with some general comments that are reasonably accurate, but you’re unlikely to get an answer that can be relied on. And with most technical commentary tied up in personal advice rather than on the web where ChatGPT can explore it, it is unlikely that we will get there any time soon.

Here are the results of our test question and our commentary (ChatGPT’s response is in italics).

Question: How much capital gains tax does an Australian resident pay on an investment property with a worked example.

ChatGPT:An Australian resident pays capital gains tax (CGT) on the profit made from selling an investment property. The CGT is calculated by subtracting the cost of the property (purchase price plus any costs associated with acquiring and owning the property) from the sale price.

For example, let’s say an Australian resident purchased an investment property for $500,000 and spent $50,000 on costs associated with acquiring and owning the property (such as legal fees, stamp duty, and repairs). The total cost of the property is $550,000.

The accountant: Let’s stop there and take stock. There are some tricks and traps that need to be considered when working out an asset’s cost base.

While repair costs in some cases can form part of a property’s cost base, this is not always the case. The situation is often different where the asset being sold is an investment property that has been rented to tenants. When a landlord repairs damage that occurs while the property is rented to a tenant, this will often be deductible to the landlord at the time the repair costs are incurred. Because deductions are available for these repair costs, they should not also be included in the property’s cost base.

There are also other adjustments that need to be considered. In the context of investment properties, it will often be necessary to make adjustments to the cost base to take into account capital works deductions. Landlords can often claim capital works deductions when an investment property is used to derive assessable rental income. The property’s cost base should then be reduced by capital works deductions that have been or could be claimed by the landlord (although there is an exception to this if the property was acquired before 13 May 1997 and the cost of improvements was incurred by 30 June 1999).

The longer the period of ownership, the more likely that capital works deductions and repair costs can end up being quite significant and have a material impact on the capital gain calculation.

ChatGPT: After several years, the resident decides to sell the property for $700,000. The profit made from the sale is $700,000 – $550,000 = $150,000.The CGT rate in Australia is currently at 45% and the resident will pay 45% of the $150,000 profit, which is $67,500.

The accountant: Let’s take a closer look at that calculation. There is no CGT rate of 45% that applies specifically to capital gains. Net capital gains form part of an individual taxpayer’s assessable income. This figure is then used to calculate the individual’s taxable income for the relevant income year. If there is a positive taxable income figure, then we apply the individual’s marginal tax rates.

One way of explaining this is that a higher taxable income normally results in a higher tax bracket and a higher rate of tax. In other words, the tax rate that applies to an individual’s net capital gains is impacted by the individual’s other income or losses (if any).

Also, while the highest marginal tax rate for individuals is currently 45 per cents for each dollar of taxable income above $180,000, Australian residents are also normally subject to the Medicare levy of 2%. This should be considered and factored in.

ChatGPT: It’s worth noting that there are certain exemptions and reductions that can be applied to the CGT calculation, such as the main residence exemption and the small business CGT concessions.

The accountant: If only tax was that simple! There are certain exemptions and reductions that can apply to capital gains. While the answer mentions the main residence exemption and the small business CGT concessions, these concessions do not normally apply to the sale of an investment property.

For the main residence exemption (or partial main residence exemption) to be available, one of the key conditions is that property would need to have been established and used as the individual’s main residence. The exemption is unlikely to be available if the property has been used solely as an investment property to derive assessable rental income, although if the property was inherited then the position could be different.

Also, the small business CGT concessions would not normally apply to the sale of an investment property. This is because the concessions can only apply if the asset passes an active asset test, which requires the property to have been used in qualifying business activities for a minimum period of time.

Assets used in a business carried on by the owner or certain related parties can often be treated as active assets for the purpose of these concessions, but there is a specific exception for assets used mainly to derive rent from unrelated parties.

If the property has been solely used to derive rent (even if used in a rental business) from unrelated parties, the property is likely to fail the active asset test and the small business CGT concessions shouldn’t be available.

Interestingly, the answer didn’t refer to the general CGT discount or indexation, which are the most likely concessions that would apply to a situation like this.

If the seller is an Australian resident (and not a temporary resident) during the period they owned the property and has owned the property for more than 12 months, the 50% CGT general discount would often be available to reduce the capital gain.

If the property was acquired before 21 September 1999, indexation of the cost base could be available instead. It would be necessary to compare both options to see which provides the more favourable result.

ChatGPT: It is advisable to consult with a tax professional to determine the specific tax implications of selling an investment property.

The accountant: Yes, indeed it is. Thank you ChatGPT.

Full throttle in 2023

In a volatile market, keeping to a strategy, or let’s face it creating one, can be tough.

The downside of not taking time out for your strategy is that there is a tendency to keep a short-term focus at an operational level to try and pick quick wins to generate financial returns. Sometimes in the process, this short-term focus undermines longer term value and returns.

Here are our ‘must dos’:

Know what your position is.

A business health check is an analysis of the current state of your business. It is an analytical review of its operation with view to providing a broad overview of operating performance and identifying potential issues. Understanding your position will reveal your risks and capacity to develop.

Know what to look for.

Once you know your position, the next question is what are the measures that are going to give you the best insight into business performance. In a volatile market, this information will give you what you need to make informed decisions at any one point in time.

Be prepared to make quick decisions.

If you know your position and have the data you need, be prepared to make quick decisions and take the first mover advantage. If you have the two elements above, you have your radar for identifying opportunities and mitigating risk. Most businesses are simply a replication of what they see. While the pandemic and market instability is difficult, we have also seen a wave of innovation as people adapt to find solutions.

Don’t bank on a single opportunity.

If COVID has taught us anything it is that things change, and we need to adapt and change with the circumstances. While one single opportunity might make all the difference, an overreliance on one product, service, or methodology of delivering those products and services, exposes you to risk.

Understand your end game.

What are you aiming for? Family empire? Fast growth and sale? Sustainable growth and sale as a retirement plan? Public listing? Even if you plan on simply running and growing your business for decades to come, that is a decision. Your end game and your progress towards that end game impacts your structure, focus, and decision making.

Document your strategy.

Document your strategy – knowing it in your head is not enough. This does not have to be an onerous War & Peace approach. It is understanding what you are aiming for, and breaking that down into measurable objectives, then into measurable outcomes and timeframes (preferably actionable against rolling 90 day plans). This approach also makes management meetings a lot more meaningful.

Is ‘downsizing’ worth it?

From 1 January 2023, those 55 and over can make a ‘downsizer’ contribution to superannuation.

Downsizer contributions are an excellent way to get money into superannuation quickly. And now that the age limit has reduced to 55 from 60, more people have an opportunity to use this strategy if it suits their needs.

What’s a ‘downsizer’ contribution?

If you are aged 55 years or older, you can contribute $300,000 from the proceeds of the sale of your home to your superannuation fund.

Downsizer contributions are excluded from the existing age test, work test, and the transfer balance threshold (but are limited by your transfer balance cap).

For couples, both members of a couple can take advantage of the concession for the same home. That is, if you and your spouse meet the other criteria, both of you can contribute up to $300,000 ($600,000 per couple). This is the case even if one of you did not have an ownership interest in the property that was sold (assuming they meet the other criteria).

Sale proceeds contributed to superannuation under this measure count towards the Age Pension assets test. Because a downsizer contribution can only be made once in a lifetime, it is important to ensure that this is the right option for you.

Let’s look at the eligibility criteria:

You are 55 years or older (from 1 January 2023) at the time of making the contribution.

The home was owned by you or your spouse for 10 years or more prior to the sale – the ownership period is generally calculated from the date of settlement of purchase to the date of settlement of sale.

The home is in Australia and is not a caravan, houseboat, or other mobile home.

The proceeds (capital gain or loss) from the sale of the home are either exempt or partially exempt from capital gains tax (CGT) under the main residence exemption, or would be entitled to such an exemption if the home was a post-CGT asset rather than a pre-CGT asset (acquired before 20 September 1985). Check with us if you are uncertain.

You provide your super fund with the Downsizer contribution into super form (NAT 75073) either before or at the time of making the downsizer contribution.

The downsizer contribution is made within 90 days of receiving the proceeds of sale, which is usually at the date of settlement.

You have not previously made a downsizer contribution to super from the sale of another home or from the part sale of your home.

Do I have to buy another smaller home?

The name ‘downsizer’ is a bit of a misnomer. To access this measure you do not have to buy another home once you have sold your existing home, and you are not required to buy a smaller home – you could buy a larger and more expensive one.

The ATO’s final position on risky trust distributions

The ATO has released its final position on how it will apply some integrity rules dealing with trust distributions – changing the goal posts for trusts distributing to adult children, corporate beneficiaries, and entities with losses. As a result, many family groups will pay higher taxes because of the ATO’s more aggressive approach.

Section 100A

The tax legislation contains an integrity rule, section 100A, which is aimed at situations where income of a trust is appointed in favour of a beneficiary, but the economic benefit of the distribution is provided to another individual or entity. For section 100A to apply, there needs to be a ‘reimbursement agreement’ in place at or before the time the income is appointed to the beneficiary. Distributions to minor beneficiaries and other beneficiaries who are under a legal disability are not impacted by these rules.

If trust distributions are caught by section 100A, this generally results in the trustee being taxed on the income at penalty rates rather than the beneficiary being taxed at their own marginal tax rates.

While section 100A has been around since 1979, until recently there has been relatively little guidance on how the ATO approaches section 100A. This is no longer the case and the ATO’s recent guidance indicates that a number of scenarios involving trust distributions could be at risk.

For section 100A to apply:

The present entitlement (a person or an entity is or becomes entitled to income from the trust) must relate to a reimbursement agreement;

The agreement must provide for a benefit to be provided to a person other than the beneficiary who is presently entitled to the trust income; and

A purpose of one or more of the parties to the agreement must be that a person would be liable to pay less income tax for a year of income.

High risk areas

Until recently many people have relied on the exclusions to section 100A which prevent the rules applying when the distribution is to a beneficiary who is under a legal disability (e.g., a minor) or where the arrangement is part of an ordinary family or commercial dealing (the ‘ordinary dealing’ exception). It is the ordinary dealing exception that is currently in the spotlight.

For example, let’s assume that a university student who is over 18 and has no other sources of income is made presently entitled to $100,000 of trust income. The student agrees to pay the funds (less tax they need to pay to the ATO) to their parents to reimburse them for costs that were incurred when the student was a minor. This situation is likely to be considered high risk if the student is on a lower marginal tax rate than the parents because the parents are receiving the real benefit of the income.

The ATO is also concerned with scenarios involving circular distributions. For example, this could occur when a trust distributes income to a company that is owned by the trust. The company then pays dividends back to the trust, which distributes some or all of the dividends back to the company. And so on. The ATO views these arrangements as high risk from a section 100A perspective.

Common scenarios identified as high risk by the ATO include:

The beneficiary is a company or trust with losses and the beneficiary is not part of the same family group as the trust making the distribution.

A company or trust which is entitled to distributions from the trust returns the funds to the trustee (i.e., circular arrangements).

The beneficiary is issued units by the trustee of the trust (or a related trust) with the amount owed for the units being set-off against the entitlement and where the market value of the units is less than the subscription price or the trustee is able to do this without the consent of the beneficiary.

Adult children are made presently entitled to income, but the funds are paid to a parent in relation to expenses incurred before the beneficiary turned 18.

Where to from here?

If you have a discretionary trust, it will be important to ensure that all trust distribution arrangements are reviewed in light of the ATO’s guidance to determine the level of risk associated with the arrangements. It is also vital to ensure that appropriate documentation is in place to demonstrate how funds relating to trust distributions are being used or applied for the benefit of the beneficiaries.

The ATO’s new approach applies to entitlements before and after the publication of the new guidance but for entitlements arising before 1 July 2022, the ATO will not generally pursue these if they are either low risk under the new guidance, or if they comply with the ATO’s previous guidance on trust reimbursement agreements.

SMSF reporting changes from 1 July 2023

If you have an SMSF with a total balance of less than $1 million, from 1 July 2023 you will need to report quarterly to the ATO instead of annually. Previously, SMSFs with a balance under $1m reported annually at the same time as lodging the SMSF annual return.

Quote of the month

“Begin with the end in mind.”

Stephen Covey

The material and contents provided in this publication are informative in nature only. It is not intended to be advice and you should not act specifically on the basis of this information alone. If expert assistance is required, professional advice should be obtained.

Market Wrap February 2023

Markets

Local: The ASX200 index fell -2.4% over February, as the RBAs 25 bps rate hike to 3.35% placed pressure on the already decelerating economy.

Global: The S&P 500 also lost momentum, dropping -2.4%. The Dow Jones Industrial Average fell -4.19% for the month and was down -1.48% YTD.

Gold: Gold prices fell strongly by US $105.25 to US $1,819, on increased scarcity driven by the sector’s requirement to replenish resource inventories of wasting assets and the lack of new discoveries.

Iron Ore: Iron Ore price fell $3.00 to US $126 /Mt on flat demand and a soft Chinese property market.

Oil: Brent Oil price also fell by $2.04 to US $82.45 /bbl fuelled by a stronger USD.

Property

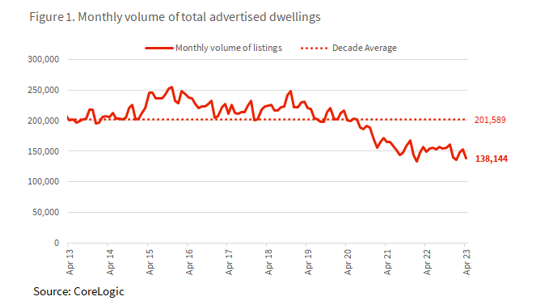

Housing: CoreLogic’s Home Value Index (HVI) recorded a sharp reduction in the rate of decline through February.

The national index declined -0.14% over the month, the smallest monthly fall since May 2022 (-0.13%), when rate hikes commenced.

A 0.3% rise in Sydney dwelling values was the most significant driver of the national deceleration, however, the loss of downwards momentum was broad-based. Darwin (-0.3%) was the only capital city to record a steeper monthly fall in February, albeit from relatively flat conditions previously. Every other capital city except Hobart (-1.4%) saw housing values fall by less than half a per cent over the month.

CoreLogic’s research director, Tim Lawless, said “The past four weeks have seen the flow of new capital city listings tracking -17.0% lower than a year ago and -11.9% below the previous five-year average, this trend towards a below average flow of new listings has been evident since September last year, coinciding with a loss of momentum in the rate of value decline.”

Economy

Interest Rates: The RBA Cash rate has now had 10 consecutive rate rises. A rise of 0.25% at the start of March has pushed the cash rate to 3.6%. Further increases are likely in the months ahead.

Retail Sales: In January retail sales in Australia rose by 1.9% MoM and rose 7.5% compared with January 2022.

Bond Yields: Australian government 10-year bond moved in reaction to tightening monetary policy, selling off 30bps to 3.86%. The US 10-year bond also sold off 39bps to 3.92%, in reaction to stronger than expected economic data.

Exchange Rate: The Aussie dollar fell over February against both the American dollar to finish the month at $0.675, and the Euro at $0.637.

Bitcoin: Bitcoin moved just 0.03% last month in US dollar terms, making February 2023 its least volatile in history. Bitcoin finished the month at US $23,410.

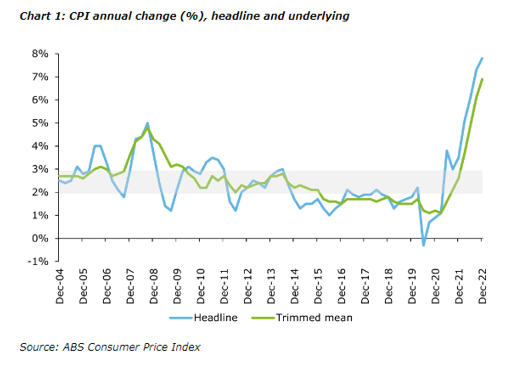

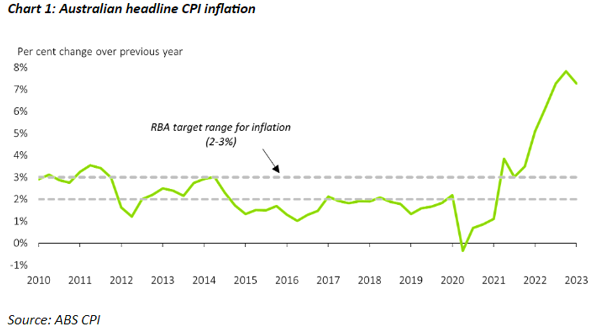

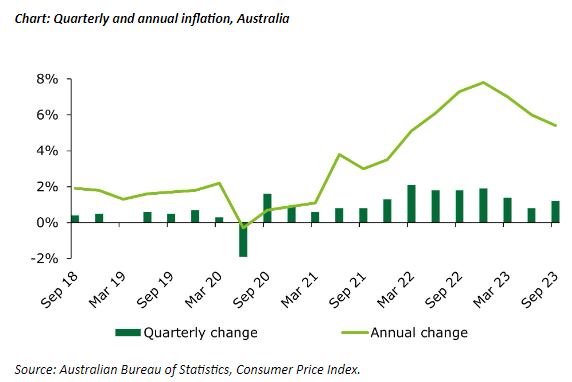

Inflation: The monthly Consumer Price Index (CPI) indicator rose 7.4% in the year to January 2023, Michelle Marquardt, ABS Head of Prices Statistics, said “This month’s annual increase of 7.4% is lower than the 8.4% rise for the year to December 2022. It is, however, the second highest annual increase since the start of the monthly CPI indicator series in September 2018, signifying ongoing high inflation.”

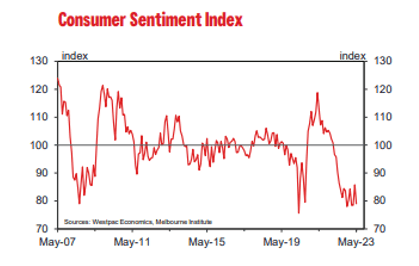

Consumer Confidence: The Westpac-Melbourne Institute Consumer Sentiment Index fell 6.9% from 84.3 in January to 78.5 in February. After a modest rally through the Christmas-New Year period, consumer confidence has fallen sharply to be back near the historic lows seen last November. Cost of living pressures and interest rate rises continue to weigh heavily. Hopes of some easing in both have been dashed by the strong December quarter CPI and the RBA’s resumption of its interest rate tightening cycle.

Employment: Australia’s seasonally adjusted unemployment rate unexpectedly increased to 3.7% in January 2023 from December’s near five-decade low of 3.5% and above market estimates of 3.5%. This was the highest jobless rate since last May, as the number of unemployed climbed by 21,900 to 523,200.

Purchasing Managers Index: The headline seasonally adjusted S&P Global Australia Manufacturing Purchasing Manager’s Index™ (PMI®) posted 50.5 in February, up from the neutral level of 50.0 in January. This signalled an improvement in the health of the Australian manufacturing sector in February, albeit only marginally.

US Services PMI: The Feb US Services PMI printed at a strong 55.1, above estimates of 54.5 and nearly the same as January. New orders, which surprised last month, rose again by 2.2 points to 62.6.

US Global Manufacturing PMI: The S&P Global Manufacturing PMI for the US was revised lower to 47.3 in February of 2023 from a preliminary of 47.8 and compared to 46.9 in January. The reading showed manufacturing activity shrank for a fourth consecutive month, amid further contractions in output and new orders, although rates slowed in both instances. Weak domestic and foreign client demand reportedly drove a further drop in total new sales as firms adjusted their spending activity and inventory holdings down accordingly.

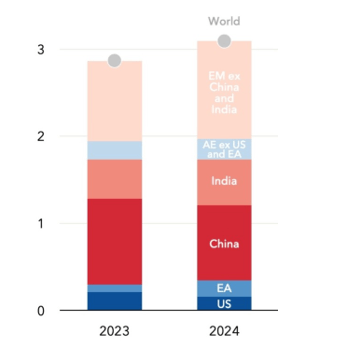

China underwent one of the world’s longest, and strictest, COVID management policies. Snap lockdowns of entire cities weakened consumer spending and disrupted supply chains were key features of the Chinese economy in 2022. This saw China’s economy grow by only 3% in 2022 – it’s worst performance in nearly half a century.

The abrupt end of China’s zero COVID policy was announced in December, and after 1,016 days China re-opened their borders to the world on the 8th of January. Already, this reopening has shifted the dial on global economic sentiment. The Economist magazine says that “China’s reopening will be the biggest economic event of 2023”. The IMF’s latest World Economic Outlook paints the outlook as ‘less gloomy’ than previously forecast, largely thanks to China’s sudden reopening.

China is expected to be a significant engine of global economic growth in 2023 and 2024. China and India alone are expected to account for around half of global growth this year, versus just a tenth for the US and Euro area combined.

Chart: Contributions to world GDP growth

Yang Jianwen, an economist at the Shanghai Academy of Social Sciences, said property and consumption were the “two biggest issues” China needed to solve. Shanghai was well-placed to tackle both, he said, adding that the city’s real estate market was “not under great pressure”.

Importantly though, consumer spending figures during the Lunar New Year period are already looking up. This is a much-needed boost for China after December retail figures contracted 1.8%, marking the third consecutive monthly decline. Box office tickets and searches for travel improved, signalling the start of a consumer bounce back over 2023 as savings loaded consumers return to old spending habits.

The rest of the world is also gearing up for China’s reopening. At an otherwise very difficult time for the global economy, the global outlook is supported by a re-engaged China. With no more restrictions, there is the potential for supply chain disruptions to ease considerably over the year.

Last week’s RBA Statement on Monetary Policy noted “the earlier opening of the Chinese economy is supporting Australia’s terms of trade and national income”.

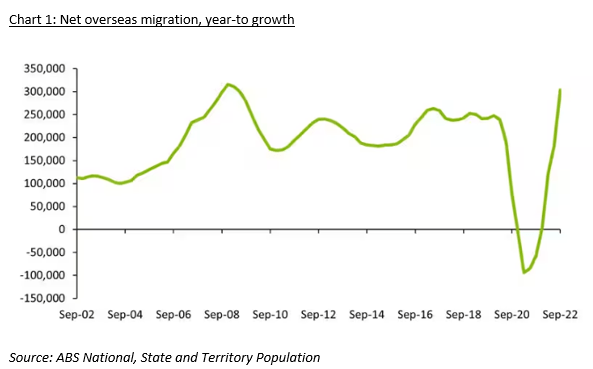

China’s reopening will also have important implications for two key exports: international education and tourism. Australia was a popular destination for both pre-COVID, with 1.4 million short term visitors from China in 2019 (an average of 120,000 per month) and 212,000 Chinese students in 2019.

COVID border closures hit tourism particularly hard with only 9,000 short term visitor arrivals from China in November 2022, only a sliver of the pre-COVID monthly average. International student numbers fell to 155,000 in 2022 as pre-COVID students finished their courses and fewer new students replaced them.

Both exports are expected to have big upsides in 2023, though the timing of this resurgence is unclear. China is facing long delays in processing passports and visas as well as sky rocketing flight prices. These are both globally competitive markets, as other countries vie for the same boost to education and tourism as Australia.

Sources:AFR, Deloitte

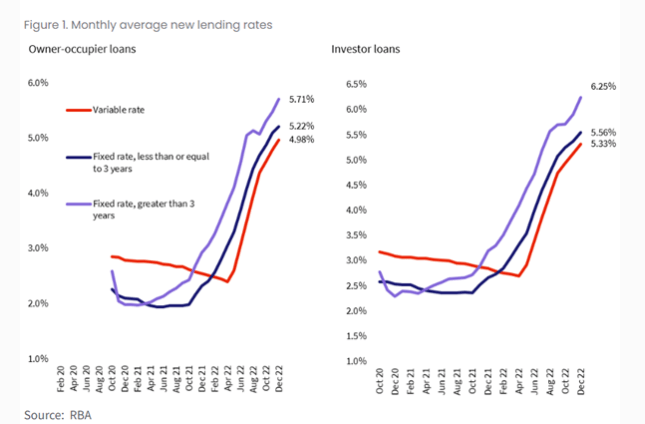

The Fixed Interest Rate Cliff

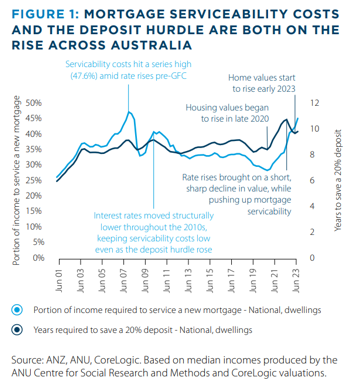

Mortgage rates fell dramatically during the pandemic. This was particularly the case for debt on ‘fixed’ terms (where payments are held steady for a specified period). Short-term fixed loan rates averaged as low as 1.95% in May 2021 for owner-occupiers, as bank funding costs plunged in line with the RBA’s temporary Term Funding Facility and fierce competition among lenders.

Fixed term home lending has historically comprised around 15% of new home loans, however as fixed interest rates plunged to record lows, fixed term home lending surged to 46.0% of new mortgage commitments in July and August of 2021. The RBA October Financial Stability Review noted that about 35% of outstanding housing credit was on fixed terms. This included the fixed component of split loans, so not all of these fixed loans represent the entire debt value of housing purchases.

The RBA noted in the Financial Stability Review that around two thirds of the 35% outstanding fixed mortgage debt would expire in 2023. Hence the ‘cliff’: around 23% of all outstanding mortgage debt will be re-priced over the course of the year, and re-priced at a much higher rate. When fixed terms come to an end, borrowers will need to refinance their loan. Factoring in another 50 basis points of rate hikes over March and April, average variable rates could be around 5.7% for owner-occupiers and over 6.0% for investors.

As more fixed loans revert to variable rates, there is likely to be some challenge to serviceability. Interest rates have risen beyond 3 percentage points for many borrowers, which is the minimum serviceability buffer recommended by APRA in assessing whether someone can repay their debt.

Stretched serviceability could be compounded by an increase in the unemployment rate this year along with higher than budgeted household costs due to high inflation. A rise in distressed sales could also put added downward pressure on property values. If people are forced to sell their home in a declining market, there is the added risk of being unable to recover mortgage debt from the sale of a home.

Looking ahead, there’s no escaping that Australians with fixed-rate loans are about to see a painful adjustment. This is partly the intention of rising rates, as households have to curb spending in response to higher interest costs. So far, listings data and arrears data suggest there is minimal impact on the housing market from defaults. However, the true test of the market will be over the next ten months.

Sources: CoreLogic, RBA

Business Matters April 2023

How Does Tax Apply to Electric Cars?

Just in time for the Fringe Benefits Tax (FBT) year that started on 1 April, the Australian Taxation Office (ATO) has released new details on electric vehicles.

The FBT exemption for electric cars

If your employer provides you with the use of a car that is classified as a zero or low emissions vehicle there is an FBT exemption that can potentially apply to the employer from 1 July 2022, regardless of whether the benefit is provided in connection with a salary sacrifice arrangement or not. The FBT exemption should normally apply where:

The value of the car is below the luxury car tax threshold for fuel efficient vehicles ($84,916 (GST Inclusive) for 2022-23) when it was first purchased. If you buy an EV second-hand, the FBT exemption will not apply if the original sales price was above the relevant luxury car tax limit; and

The car is both first held and used on or after 1 July 2022. This means that the car could have been purchased before 1 July 2022, but might still qualify for the FBT exemption if it wasn’t made available to employees until 1 July 2022 or later.

The exemption also includes associated benefits such as:

Registration

Insurance

Repairs or maintenance, and

Fuel, including electricity to charge and run the vehicle.

But, it does not include a charging station (see How do the tax rules apply tohome charging units?).

While the FBT exemption on EVs applies to employers, the value of the fringe benefit is still taken into account when working out the reportable fringe benefits of the employee. That is, the value of the benefit is reported on the employee’s income statement. While you don’t pay income tax on reportable fringe benefits, it is used to determine your adjusted taxable income for a range of areas such as the Medicare levy surcharge, private health insurance rebate, employee share scheme reduction, and certain social security payments.

Who the FBT exemption does not apply to

By its nature, the FBT exemption only applies where an employer provides a car to an employee. Partners of a partnership and sole traders are not employees and cannot access the exemption personally.

If you are a beneficiary of a trust or shareholder of a company, the exemption can only apply if the benefit is provided in your capacity as an employee or as a director of the entity (you need to be able to show you have an active role in the running of the entity).

How do the tax rules apply to home charging units?

The ATO has confirmed that charging stations don’t fall within the scope of the FBT exemption for electric cars. This means that FBT could be triggered if an employer provides a charging unit to an employee.

If an employee purchases a home charging unit then it might be possible to claim depreciation deductions for the cost of the unit over a number of income years if the unit is used to charge a vehicle that is used for income producing purposes. However, if an employee is only using the vehicle for private purposes then the cost of the charging unit is a private expense and not deductible.

What about the cost of electricity?

A friend of mine travels a lot for work and used to rack up large travel expenses…right up until he switched to an electric vehicle. Now it costs him 3 cents per km in electricity.

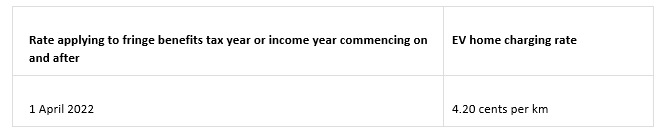

Because it is often difficult to distinguish home electricity usage, the ATO has set down a rate of 4.20 cents per km for running costs for EVs provided to an employee (from 1 April 2022 for FBT and 1 July 2022 for income tax).

If you use this rate, you cannot also claim any of the costs associated with costs incurred at commercial charging stations. It is one or the other, not both.

You also have the option of using actual electricity costs if you can calculate them accurately.

Selling a business? The pros and cons of earn-out clauses

Earn-out clauses for the sale of a business are increasingly common. We look at the positives and negatives that every business owner should consider.

Business transactions often include earn-out clauses where the vendors ‘earn’ part of the purchase price based on the performance of the business post the transaction. Typically, an earn-out will run for a period of one to three years post transaction date.

There are two main reasons to include an earn-out in a sale:

To bridge a gap in the sale price expectations between the vendor and the purchaser. The earn out represents an ‘at risk’ form of consideration. If the business produces the result, the vendors are rewarded through a higher sale price.

To incentivise the vendors who are continuing to work in the business and maintain the growth momentum of the business post sale.

Advantages of earn-outs include:

The ultimate sale price has a performance component to it – both buyer and seller benefit.

May assist in achieving a sale where a price impasse would otherwise prevent the sale.

If the calculation of the earn-out is transparent and easily measurable, there should be no dispute between the parties.

Creates equity where the business has lagging income, new business initiatives in play at the time of sale or a high growth rate.

The incremental sale price can be effectively funded by the business out of realised growth.

The key to an effective earn-out is in their construction, both from a commercial and a legal perspective. Get them right and they can enhance the continuity and succession of a business.

What sharing platforms are sharing with the ATO

From 1 July 2023, a new reporting regime will require platforms that enable taxi services including ride sourcing, and short-term accommodation to report their transactions to the ATO each year. From 1 July 2024, the regime will expand to include all other platforms.

While the legislative instrument for the reporting regime is still in draft (see LI 2022/D27), it is expected that platform providers will report their transactions to the ATO every six months.

What information on sellers will the ATO know?

The platforms will submit data on the sellers for transactions on their platform including:

ABN and business / trading name (where applicable)

First, middle and surname/family name (for individuals)

Date of birth (for individuals)

Residential or business address

Email address and telephone numbers

Bank account details.

And, for platforms facilitating short-term accommodation:

Listed property name

Listed property address

Number of nights booked.

In addition, the platforms will provide aggregate quarterly data on the value of transactions, industry types, total gross income etc.

The reporting regime does not include platforms that simply match suppliers to sellers and are not engaged in the transaction such as quotes for hiring tradies where the job is not accepted through the website.

Company money: A guide for owners for owners

When you start up a business, inevitably, it consumes not just a lot of time but a lot of cash and much of this is money you have already paid tax on. So, it only seems fair that when the business is up and running the business can pay you back. Right?

There a myriad of ways owners look for payback from a company they have invested their time and money into it from dividends, salary and wages, jobs for sometimes underqualified family members to cash advances and personal expenses like school fees and nights out picked up as a company expense. But, once the cash is in the company, it is company money.

We look at the flow of money in and out of a company and the problems that trip business owners up.

Repaying money loaned to the company

If you have lent money to your company, you can draw this money back out as a loan repayment. The loan repayment is not deductible to the company but any interest payments made to you will be as long as the borrowed money has been used in the company’s business activities (assuming interest has actually been charged on the loan).

Conversely, any repayments made by the company on the loan principal are not income for tax purposes but you will need to declare any interest earned in your income tax return. All loans, including the loan term and repayments, should be documented.

Dividends: Paying out profits

Dividends basically represent company profits being paid out to the shareholders of a company. If the company has franking credits from income tax it has paid, the dividends might be franked and the credits can often be used by the shareholder to reduce their personal tax liability.

When a dividend is paid by a private company it must provide a distribution statement to the shareholders within four months after the end of the financial year. This gives private companies up to four months after the end of the financial year to work out the extent to which dividends will be franked.

If any of the shares in the company are held by a discretionary trust then there are some additional issues that will need to be considered, including whether the trust has a positive amount of net income for the year, whether the trust has made a family trust election for tax purposes and who will become entitled to distributions made by the trust for that year.

Repaying share capital

Many private companies are set up with a relatively small amount of share capital. However, if a company has a larger share capital balance then there might be scope for the company to undertake a return of share capital to the shareholders. Whether this is possible will depend on the terms of the company constitution and there are some corporate law issues that need to be addressed.

From a tax perspective, a return of share capital will normally reduce the cost base of the shares for CGT purposes, which means that a larger capital gain could arise on future sale of the shares but there won’t necessarily be an immediate tax liability. Having said that, there are some integrity rules in the tax system that need to be considered. The risk of these rules being triggered tends to be higher if the company has retained profits that could be paid out as dividends.

Shareholder loans, payments and forgiven debts: Using company money

There are some rules in the tax law (known as Division 7A) that determine how money taken out of a company is treated. Division 7A is a particularly tricky piece of tax law designed to prevent business owners accessing funds in a way that circumvents income tax. While amounts taken from a company bank account by the owners are often debited to a shareholder’s loan account in the financial statements, Division 7A ensures that any payments, loans, or forgiven debts are treated as if they were dividends for tax purposes unless there is a loan agreement in place which meets certain strict requirements. These ‘deemed’ dividends cannot normally be franked.

If you have taken money out of the company bank account then the main ways of avoiding this deemed dividend from being triggered are to ensure that the loan is fully repaid or placed under a complying loan agreement before the earlier of the due date and actual lodgement date of the company’s tax return for that year. To be a complying loan agreement the agreement requires minimum annual repayments to be made over a set period of time and there is a minimum benchmark interest rate that applies – currently 4.77% for 2022-23.

For example, if your company is paying school fees for your kids, or you take money out of the company bank account to pay down your personal home loan, if you don’t pay back this amount or put a complying loan agreement in place then this amount is likely to be treated as a deemed unfranked dividend. That is, you need to declare this amount in your personal income tax return as if it was a dividend and without the benefit of any franking credits. This means that even though the company might have already paid tax on this amount, you will be taxed on it again without the ability to claim a credit for the tax already paid by the company (causing double taxation of the same company profits).

The rules are very strict when it comes to loan repayments. If a repayment is made but the same amount or more is loaned to the shareholder shortly afterwards then there are some special rules that can apply to basically ignore the repayment. There are some exceptions to these rules and the position needs to be managed carefully to avoid adverse tax implications.

Update: Tax on super balances above $3m

In a very quick turnaround from announcement to draft legislation, Treasury has released the exposure draft legislation for consultation to enact the Government’s intention to impose a 30% tax on future superannuation fund earnings where the member’s total superannuation balance is above $3m.

The draft legislation confirms the Government’s intention to:

Impose the tax on member accounts with superannuation balances above $3 million from 1 July 2025 (not indexed); and

Apply the additional 15% tax to ‘unrealised gains’. This will mean that a tax liability will arise if the value of the assets goes up

Currently, all fund income is taxed at either 15%, or 10% for capital assets that have been held by the fund for more than 12 months. Unrealised gains, that is gains that are made because of changes in value, gains on paper, are not currently taxed – only when the gain is realised on sale or disposal of the asset.

If enacted, the legislation would mean that those impacted, could be paying tax on gains in value but without the cash from a sale to support the tax payment.

Budget 2023-24

The 2023-24 Federal Budget will be released on Tuesday, 9 May 2023. Look out for our update the next day on the important issues to you, your superannuation and your business.

Little has been released to date on the impending Budget beyond the tax on super balances above $3m and the decision not to extend the temporary $1,500 low and middle income tax offset beyond 30 June 2023.

Cost of living is a focus but on this, the Government is walking a tightrope between easing pressure without increasing inflation.

In the election cycle, if there is going to be a tightening, the mid-term Budgets are the time to do it. The Government will undoubtedly look at concessions provided within the tax system and whether those concessions meet their stated objective and when it comes to spending, potentially redraw the allocations. Some of the areas to watch include:

The legislated stage three tax cuts, that collapse the 32.5% and 37% tax brackets to a single rate of 30% for those with assessable income between $45,000 and $200,000 are not due to commence until 1 July 2024. The Government committed to keeping the tax cuts during the election and can bypass the issue until the 2024-25 Budget, but we’ll see.

Provision for announced defence spending.

Active support to develop a viable clean energy industry and transition to clean energy (see the joint submission from the Business Council of Australia, Australian Council of Trade Unions, World Wide Fund for Nature-Australia and the Australian Conservation Foundation).

Productivity measures – Temporary full expensing – the productivity measure designed to encourage business investment that enables a business to fully expense the cost of depreciable assets in the first year of use – is set to expire on 30 June 2023. The Government will either extend, redevelop the small business instant asset write-off, or remove the concession altogether.

Technology and training boosts – In the 2022-23 Federal Budget, the former Government announced that it would provide certain business taxpayers with ‘bonus’ tax deductions for investing in employee training or improving digital operations. The Skills and Training Boost allows small businesses (aggregated turnover less than $50 million) to claim a 120% deduction for eligible expenditure incurred on external training for employees between 29 March 2022 and 30 June 2024. The Technology Investment Boost provides a 120% deduction for eligible expenses that are incurred for the purposes of improving digital operations or digitising business operations. This can include the cost of depreciating assets. The boost is aimed at costs incurred between 29 March 2022 and 30 June 2023 and is limited to a maximum bonus deduction of $20,000. But, the legislation enabling both boosts has not passed Parliament. There is an opportunity in the Budget to extend the scope and nature of the concession.

Note: The material and contents provided in this publication are informative in nature only. It is not intended to be advice and you should not act specifically on the basis of this information alone. If expert assistance is required, professional advice should be obtained.

2023-2024 Budget

‘Ace in the Hole’ Budget 2023-24

The ‘ace in the hole’ of the 2023-24 Federal Budget was the $4.2bn surplus; the first in 15 years.

The surplus was driven by a surge in the corporate and individual tax take. High commodity prices, inflation, and high employment have all pushed up corporate and individual tax receipts. But the gains can’t be relied on long term. The Budget is expected to deliver a deficit of $13.9 billion in 2023-24, and a $35.1bn deficit in 2024-25.

Social initiatives dominated the Budget:

Energy bill relief for some households and small business

Encouraging doctors to offer bulk billing by tripling the incentive for children under 16, pensioners and other Commonwealth card holders

Increases to commonwealth rent assistance

Increases to JobSeeker and other income support payments

Expanding access to the single parenting payment

The legislated stage 3 tax cuts legislated to take effect on 1 July 2024 remain in place. Stage 3 radically simplifies the tax brackets by collapsing the 32.5% and 37% rates into a single 30% rate for those earning between $45,001 and $200,000.

For small business, the instant asset write-off will enable multiple assets of up to $20,000 to be written-off in the year of purchase.

What wasn’t in the Budget?

There was no mention of the loss carry back rules for companies, suggesting that these rules will expire on 30 June 2023, along with the temporary full expensing rules. The loss carry back rules allow eligible companies to apply tax losses against taxable profits made in certain previous income years, rather than carrying them forward to future years.

There is no mention of the simplification of Division 7A – Division 7A captures situations where shareholders access company profits in the form of loans, payments or the forgiveness of debts. The 2016-17 Federal Budget proposed changes to reduce the compliance burden of Division 7A. These changes were initially meant to apply from 1 July 2018 but were deferred a number of times, before the Government announced that any changes would commence from the start of the income year following the date on which the changes receive Royal Assent. Aside from a Treasury discussion paper released back in October 2018, this issue remains in limbo.

The Budget also doesn’t refer to either the Skills and Training Boost or the Technology Investment Boost. These measures, announced by the previous Government, would provide a bonus deduction equal to 20% of qualifying expenditure if the legislation containing these measures is passed in its current form (Treasury Laws Amendment (2022 Measures No. 4) Bill 2022). The Technology Investment Boost is aimed at expenditure incurred between 7:30pm (ACT) on 29 March 2022 and 30 June 2023. The Skills and Training Boost is aimed at expenditure incurred between 7:30pm (ACT) on 29 March 2022 and 30 June 2024.

If we can assist you to take advantage of any of the Budget measures, or to risk protect your position, please let us know.

As always, we’re here if you need us!

Doug Tarrant

Principal

Level One Business and Financial Advisers

T: 02 4227 6744

E:

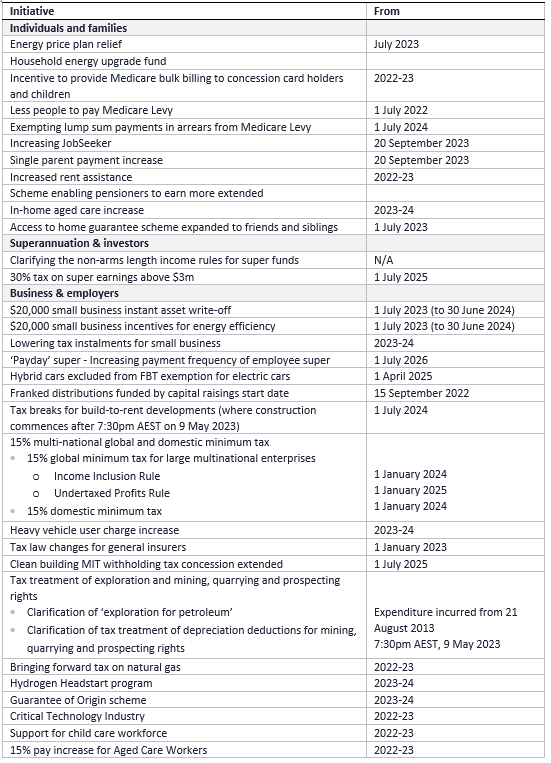

Individuals & families

Energy price plan relief

From

July 2023

$1.5bn has been provided over 5 years to provide targeted energy bill relief and progressing gas market reform.

The Energy Bill Relief Fund will provide targeted energy bill relief to eligible households and small business customers, which includes pensioners, Commonwealth Seniors Health Card holders, Family Tax Benefit A and B recipients and small business customers of electricity retailers.

In partnership with the states and territories, the plan is expected to deliver up to $500 in electricity bill relief for eligible households and up to $650 for eligible small businesses.

Funding has also been provided to the ACCC to enforce the temporary cap of $12 per gigajoule on the price of gas and to develop and implement a mandatory gas code of conduct. And, funding for Australian Energy Regulator to monitor coal and gas markets across the National Electricity Market.

The Government expects that retail electricity price increases in 2023-24 will be around 25% smaller and retail gas price increases around 16% smaller as a result of their interventions.

Household energy upgrade fund

A $1.3bn Household Energy Upgrades Fund will be established to support home upgrades that improve energy performance. No, the Government is not giving out cash for upgrades but providing $1bn to the Clean Energy Finance Corporation to provide low-cost finance and mortgages in partnership with private financial institutions for home upgrades that save energy.

$300m is committed to upgrading social housing in collaboration with states and territories. And, over $36m to upgrade the energy ratings systems.

Incentive to provide Medicare bulk billing to concession card holders and children

From

2022-23

As previously announced, the bulk billing incentive benefits for consultations for Commonwealth concession card holders and patients aged under 16 years of age will be tripled from 2022-23.

Less people to pay Medicare Levy

From

1 July 2022

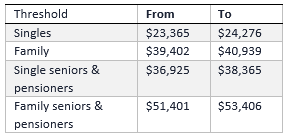

The Medicare levy low-income thresholds for singles, families and seniors and pensioners will increase from 1 July 2022.

For each dependent child or student, the family income thresholds will increase by a further $3,760 instead of the previous amount of $3,619.

Exempting lump sum payments in arrears from Medicare Levy

The Government will introduce a technical amendment to ensure that low income earners who receive eligible lump sum payments are not subject to a higher amount of the Medicare Levy. For example, if an individual receives a lump sum compensation payment for underpaid wages.

To qualify, taxpayers must be eligible for a reduction in the Medicare levy in the 2 most recent years to which the lump sum accrues. Taxpayers must also satisfy the eligibility requirements of the existing lump sum payment in arrears tax offset, including that a lump sum accounts for at least 10% of the taxpayer’s income in the year of receipt.

Increasing JobSeeker

The Government will increase support for people receiving working age payments including JobSeeker.

The base rate of working age and student payments will increase by $40 per fortnight from 20 September 2023. The increase applies to the JobSeeker Payment, Youth Allowance, Parenting Payment (Partnered), Austudy, ABSTUDY, Disability Support Pension (Youth), and Special Benefit.

In addition, eligibility for the existing higher single JobSeeker Payment rate for recipients aged 60 years and over will be extended to recipients aged 55 years and over who are on the payment for 9 or more continuous months.

Single parent payment increase

From

20 September 2023

As previously announced, the age cut-off for the Parenting Payment (Single) will increase from 8 to 14.

From 20 September 2023, (subject to the passage of legislation), single parents will no longer have to transfer to JobSeeker when their youngest child turns eight. Instead, they will continue to receive the higher support, with a current base rate of $922.10 per fortnight until their youngest child turns 14.

As a result, eligible single parents currently on JobSeeker will receive an increase to payments of $176.90 per fortnight.

Single parents moving to Parenting Payment (Single) will also benefit from more generous earning arrangements compared to JobSeeker. Eligible single parents with one child will be able to earn an extra $569.10 per fortnight, plus an extra $24.60 per additional child, before their payment stops.

The maximum rates of the Commonwealth Rent Assistance (CRA) allowances will increase by 15% from 2022-23.

Scheme enabling pensioners to earn more extended

The measure enabling age pensioners and veterans to earn more money before their pension is reduced has been extended for another 6 months, until 31 December 2023.

Under this measure, pensioners can earn up to $11,800 before their pension is reduced.

In-home aged care increase

An additional 9,500 Home Care Packages will be available in 2023-24. The $338.7m package also includes a trial to test products and services for a new assistive technologies loan program, commencing in July 2024 within 2 states and territories.

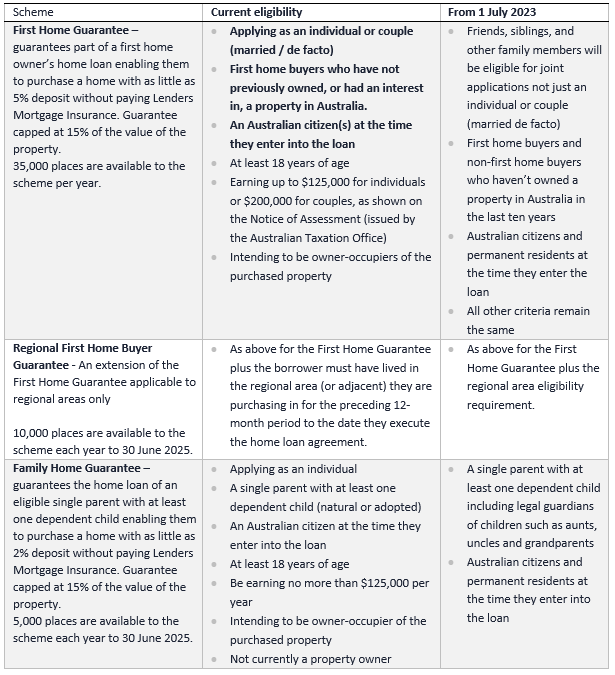

Access to home guarantee scheme expanded to friends and siblings

As previously announced, from 1 July 2023, access to the Government’s Home Guarantee Scheme will be expanded to joint applications from “friends, siblings, and other family members” and to those who have not owned a home for at least 10 years.

Superannuation & investors

Clarifying the non-arms length income rules for super funds

The non-arms length income (NALI) rules prevent superannuation trustees artificially increasing the balance of the fund, and accessing preferential tax treatment on the higher amount, by failing to recognise expenses incurred by the fund provided by a related party at a reduced rate. For example, your brother is a qualified accountant and does all of your SMSF’s accounting work for free (that he would normally charge $5k for).

Currently, where expenses incurred by the fund are not at arm’s length and below market rates, any income derived could be deemed to be non-arm’s length income and taxed at the top marginal tax rate. Expenses are divided into two categories, general and specific. General expenses relate to all of the income of the fund, for example accounting and audit fees. Specific expenses relate to a specific asset such as maintenance expenses on a property owned by an SMSF.

A Treasury consultation paper released in January 2023 recommended amendments to the way NALI is dealt with. The consultation recommended capping the amount of fund income taxable as NALI to 5 times the amount of the breach. The Budget confirms this cap to twice the level of a general expense.

In addition, fund income taxable as NALI will exclude contributions.

Expenditure that occurred prior to the 2018-19 income year will be exempt.

And, as per the consultation, large APRA regulated funds will be exempted from the NALI provisions for both general and specific expenses of the fund.

Confirmed 30% tax on super earnings above $3m

From

1 July 2025

An additional tax of 15% on earnings will apply to individuals with a total superannuation balance over $3 million at the end of a financial year from 1 July 2025. The definition of total superannuation balance (TSB) for the new tax uses the current definition and includes amounts in retirement phase pensions.

The calculation for the tax aims to capture growth in TSB over the financial year allowing for contributions (including insurance proceeds) and withdrawals. This method captures both realised and unrealised gains, enabling negative earnings to be carried forward and offset against future years.

Interests in defined benefit schemes will be appropriately valued and will have earnings taxed under this measure in a similar way to other interests.

Individuals will have the choice of paying the tax personally or from their superannuation fund and those with multiple accounts can nominate which fund will pay the tax.

This measure is estimated to increase tax receipts by $950m and increase payments by $47.6m over the 5 years from 2022-23.

Business & employers

$20,000 small business instant asset write-off

From

1 July 2023 to 30 June 2024

Small businesses, with an aggregated turnover of less than $10 million, will be able to immediately deduct the full cost of eligible depreciating assets costing less than $20,000 that are first used or installed ready for use between 1 July 2023 and 30 June 2024.

“Immediately deductible” means a tax deduction for the asset can be claimed in the same income year that the asset was purchased and used (or installed ready for use).

If the business is registered for GST, the cost of the asset needs to be less than $20,000 after subtracting the GST credits that can be claimed for the asset. If the business is not registered for GST, it is $20,000 including GST.

The write-off applies per asset, so a small business can deduct the cost of multiple assets.

The rules only apply to assets that fall within the scope of the depreciation provisions. Expenditure on capital improvements to buildings that falls within the scope of the capital works rules is not expected to qualify.

Assets valued at $20,000 or more (which cannot be immediately deducted) can continue to be placed into the small business simplified depreciation pool and depreciated at 15% in the first income year and 30% each income year thereafter.

The provisions that prevent small businesses from re-entering the simplified depreciation regime for 5 years if they opt-out will continue to be suspended until 30 June 2024. This will be particularly relevant to small business entities that chose to leave the simplified depreciation system in order to opt-out of applying the temporary full expensing rules to one or more specific assets.

This announcement effectively confirms that the temporary full expensing rules, which have provided an immediate deduction for the full cost of assets acquired from 6 October 2020, will come to an end on 30 June 2023. Small business entities that are considering acquiring depreciating assets with a cost of $20,000 or more and business entities with aggregated turnover of $10 million or more should keep this cut-off date in mind as 30 June 2023 approaches.

$20,000 small business incentives for energy efficiency

Date

1 July 2023 to 30 June 2024

As previously announced, the Small Business Energy Incentive provides an additional deduction of 20% of the cost of eligible depreciating assets that support electrification and more efficient use of energy.

Up to $100,000 of total expenditure will be eligible, with a maximum bonus deduction of $20,000.

The incentive is available to small and medium businesses with aggregated annual turnover of less than $50 million.

While the full detail of what qualifies for the incentive is not yet available, it is expected to apply to a range of depreciating assets and upgrades to existing assets such as electrifying heating and cooling systems, upgrading to more efficient fridges and induction cooktops, and installing batteries and heat pumps.

Some exclusions will apply including electric vehicles, renewable electricity generation assets, capital works, and assets that are not connected to the electricity grid and use fossil fuels.

Eligible assets or upgrades will need to be first used or installed ready for use between 1 July 2023 and 30 June 2024 to qualify for the bonus deduction.

Normally, GST and PAYG instalment amounts are adjusted using a GDP adjustment or uplift.

In 2022-23, the Government reduced this uplift factor to 2% instead of the 10% rate that would have applied. And now for 2023-24, the Government has set the uplift factor to 6% instead of the 12% rate that would have applied.

The 6% uplift rate will apply to small to medium enterprises eligible to use the relevant instalment methods for instalments for the 2023-24 income year and are due after the amending legislation comes into effect:

Up to $10 million annual aggregated turnover for GST instalments, and

$50 million annual aggregated turnover for PAYG instalments.

‘Payday’ super – Increasing payment frequency of employee super

Date

1 July 2026

As previously announced, from 1 July 2026, employers will be required to pay their employees’ super guarantee entitlements on the same day that they pay salary and wages.

Currently, SG is paid quarterly.

The Government will undertake a consultation process with the aim of providing details of the final design of the measure in the 2024-25 Federal Budget.

Hybrid cars excluded from FBT exemption for electric cars

Date

1 April 2025

As previously announced, plug-in hybrid electric cars will be excluded from the fringe benefits tax (FBT) exemption for eligible electric cars from 1 April 2025.

Arrangements entered into between 1 July 2022 and 31 March 2025 can remain eligible for the FBT exemption as long as the exemption applied to the car before 1 April 2025 and the employer has a financially binding commitment to continue providing private use of the car on and after this date.

Franked distributions funded by capital raisings start date

Date

15 September 2022

In 2016-17, the Government announced that it would seek to prevent shareholders from taking advantage of franking credits attached to dividends that are funded by capital raisings. The Budget confirms the Government’s intention to pursue this measure with a revised start date of 15 September 2022.

Under the measure, a distribution (dividend) paid by an entity will be treated as being funded by capital raising if:

The distribution is not consistent with an established practice of the entity of making distributions of that kind on a regular basis;

There is an issue of equity interests in the entity; and

It is reasonable to conclude, having regard to all relevant circumstances, that either:

The principal effect of the issue of any of the equity interests was to directly or indirectly fund all or part of the distribution; or

An entity that issued or facilitated the issue of the interests did so for a purpose of funding all or part of the distribution.

The proposed changes seek to prevent the use of artificial arrangements where capital is raised to fund the payment of franked dividends to shareholders and therefore enable the distribution of franking credits. The Government is concerned that these arrangements can involve a manipulation of the system to allow existing shareholders to obtain the benefit of both the franking credits and the profits that generated those credits being retained in the company.

The effect of the proposed amendments is that direct or indirect recipients of affected dividends are not entitled to a tax offset, and the amount of the franking credit is not included in the assessable income of the recipient. The dividends are also not exempt from non-resident withholding tax.

The application date of the original measure was to be 19 December 2016. It has now shifted to 15 September 2022.

As previously announced, the Government is actively sweetening the deal for build-to-rent developments.

For eligible new build-to-rent projects where construction commences after 7:30pm AEST on 9 May 2023, the Government will:

Increase the rate for the capital works tax deduction (depreciation) from 2.5% to 4% p.a.

Reduce the final withholding tax rate on eligible fund payments from managed investment trust (MIT) investments from 30% to 15%.

The measure applies to build-to-rent projects where 50 or more apartments are made available to rent to the general public. The dwellings must be retained under single ownership for at least 10 years before being able to be sold and landlords must offer a lease term of at least 3 years for each dwelling.

The reduced MIT withholding tax rate for residential build-to-rent will apply from 1 July 2024. The Government will work through a consultation process to determine implementation details, including any minimum proportion of dwellings being offered as affordable tenancies and the length of time dwellings must be retained under single ownership.

The tobacco excise and excise-equivalent customs duty will increase by 5% per year for 3 years from 1 September 2023 in addition to ordinary indexing.

In addition, the duty on products subject to the per kilogram excise and excise-equivalent customs duty (i.e., roll-your-own tobacco), will increase. The ‘equivalisation weight’ will be progressively lowered from 0.7 to 0.6 grams on 1 September each year from 2023, with the new weight coming fully into effect from 1 September 2026.

The measure is expected to increase receipts by $3.3bn and increase GST payments to the states and territories by $290m over the 5 years from 2022-23.

15% multi-national global and domestic minimum tax

The Government will implement key aspects of the OECD’s Two Pillar Solution introducing:

A 15% global minimum tax for large multinational enterprises with the Income Inclusion Rule applying to income years starting on or after 1 January 2024 and the Undertaxed Profits Rule applying to income years starting on or after 1 January 2025.

A 15% domestic minimum tax applying to income years starting on or after 1 January 2024.

The tax is based on the OECD Global Anti-Base Erosion Model Rules, which are designed to ensure large multinationals pay an effective minimum level of tax on the income arising in each jurisdiction where they operate.

The global minimum tax rules would allow Australia to apply a top up tax on a resident multinational parent or subsidiary company where the group’s income is taxed below 15%.

The global minimum tax and domestic minimum tax will apply to large multinationals

with annual global revenue of EUR750 million (approximately $1.2 billion) or more.

Heavy vehicle user charge increase

From

2023-24

The Heavy Vehicle Road User Charge rate from 27.2 cents per litre of diesel by 6% per year over 3 years from 2023-24 to 32.4 cents per litre in 2025-26.

Tax law changes for general insurers

From

1 January 2023

The introduction of the new accounting standard, AASB17 Insurance Contracts, by the Australian Accounting Standards Board, has meant that the tax law is no longer aligned with accounting standards. A legislative amendment will be made to enable general insurers to continue to use audited financial reporting information, which is calculated according to the new standard, as the basis for their tax returns.

Clean building MIT withholding tax concession extended

From

1 July 2025

The clean building managed investment trust (MIT) withholding tax concession will be extended to eligible data centres and warehouses that meet the relevant energy efficiency standard, where construction commences after 7:30pm AEST on 9 May 2023.

This measure will also raise the minimum energy efficiency requirements for existing and new clean buildings to a 6-star rating from the Green Building Council Australia or a 6-star rating under the National Australian Built Environment Rating System. The Government will consult on transitional arrangements for existing buildings.

Tax treatment of exploration and mining, quarrying and prospecting rights

From

Expenditure incurred from 21 August 2013

As previously announced, the Government will amend the Petroleum Resource Rent Tax (PRRT) to clarify that ‘exploration for petroleum’ is limited to the ‘discovery and identification of the existence, extent and nature of the petroleum resource’ and does not extend to ‘activities and feasibility studies directed at evaluating whether the resource is commercially recoverable’.

From

7:30pm AEST, 9 May 2023

The tax treatment of depreciation deductions for mining, quarrying and prospecting rights will also be clarified to ensure that deductions will only commence when they are used (not merely held).

Bringing forward tax on natural gas

As previously announced, the Government will amend the Petroleum Resource Rent Tax (PRRT) to limit deductions and introduce a series of integrity measures for the offshore LNG industry. Consultation on the changes will occur later in 2023.

This measure is estimated to increase receipts by $2.4bn over the 5 years from 2022-23. The ATO will also be provided with $4.4 million to administer and ensure compliance.

Picking winners: Hydrogen industry

Over $2bn has been committed to accelerate the development of Australia’s hydrogen industry, catalyse clean energy industries, and help Australia connect to new global hydrogen supply chains.

The Hydrogen Headstart program will provide revenue support for investment in renewable hydrogen production through competitive production contracts, including funding for the Australian Renewable Energy Agency and the Department of Climate Change, Energy, the Environment and Water to support the development and operation of the program.

In a separate program, $38.2m has been provided for a Guarantee of Origin scheme, which will certify renewable energy and track and verify emissions from clean energy products – in particular hydrogen from 2023-24.

$116m over 5 years will support the development of critical technologies. This includes support for businesses to integrate quantum and artificial intelligence (AI) technologies into their operations through:

A Critical Technologies Challenge Program supporting projects that use critical technologies to solve significant national challenges, and will commence with a focus on projects that use quantum computing

Extending the National AI Centre and its role in supporting responsible AI usage

Establishing an Australian Centre for Quantum Growth to support ecosystem growth and commercialisation in Australia’s quantum industry

Supporting SME’s adoption of AI technologies to improve business processes and increase trade competitiveness.

In addition, a Powering Australia Industry

Growth Centre will develop advanced technology and skills as part of the Government’s Australian Made Battery Plan.

Support for child care workforce

From

2022-23

A series of measures will support the Early Childhood Education and Care (ECEC) sector including:

$34.4m over 5 years to subsidise ECEC services to backfill up to 75,000 early childhood educators, and training for teachers and directors.

$33.1m over 5 years for financial assistance for up to 6,000 educators to undertake a paid practicum in initial teacher education courses at a bachelor or post-graduate level.

$4.8m for up to 2,000 ECEC workers to undertake a practicum exchange at a different service.

15% pay increase for Aged Care Workers

From

2022-23

$515m over 5 years will be provided to fund the outcome of the Fair Work Commission’s decision on the Aged Care Work Value Case – increasing award wages by 15% from 30 June 2023 for many aged care workers including registered nurses, enrolled nurses, assistants in nursing, personal care workers, home care workers, recreational activity officers, and some head chefs and cooks.

The increase will be partially offset by a temporary reduction in the residential aged care provision ratio from 78 places to 60.1 places per 1,000 people aged over 70 years.

Scrapped ‘Patent Box’ regime

The Patent Box regime was to provide a concessional effective corporate tax rate of 17% on income derived from patents, to the extent that the taxpayer undertakes the R&D of that patent in Australia. The patent box tax regime was originally announced for the medical and biotech industries, and later extended to agriculture and emissions.

All ‘patent box’ measures have now been scrapped.

Delayed Streamlining excise administration for fuel and alcohol

From

1 July 2024

The start date for the 2022-23 March Budget measure to streamline fuel and alcohol excise compliance has been pushed back to 1 July 2024.

Film industry location offset

To attract investment from large-budget screen productions and provide domestic employment and training opportunities, the Location Offset rebate rate will increase to 30%, whilst increasing the minimum Qualifying Australian Production Expenditure thresholds to $20m for feature films and $1.5m per hour for television series.

Government & regulators

Extending Part IVA anti-avoidance rules

From

1 July 2024

Part IVA is the general anti-avoidance provision that the ATO can use to attack arrangements that are entered into in order to obtain tax benefits.

The scope of Part IVA will be extended so that it can apply to:

Schemes that reduce tax paid in Australia by accessing a lower withholding tax rate on income paid to foreign residents

Schemes that achieve an Australian income tax benefit, even where the dominant purpose was to reduce foreign income tax.

This measure will apply to income years commencing on or after 1 July 2024, regardless of whether the scheme was entered into before that date.

AAT to be replaced

The Administrative Appeals Tribunal will be replaced by a new federal administrative review body. Funding has been provided to appoint new members to the AAT to address the backlog, to manage the transition, and to develop a modern case management system for the new body.

Small business ATO compliance

Among the programs to reduce the compliance burden on small business is a series of initiatives to cut paperwork. These include:

From 1 July 2024, small businesses will be permitted to authorise their tax agent to lodge multiple Single Touch Payroll forms on their behalf.

From 1 July 2024, the Australian Taxation Office (ATO) will reduce the use of cheques for income tax refunds.

From 1 July 2025, small businesses will be permitted up to 4 years to amend their income tax returns (generally 2 years).

Personal income tax compliance and rental property owners under scrutiny

From

1 July 2025

The ATO will receive $89.6m and Treasury $1.2m over two years to extend the personal income tax compliance program for two years and to expand it to target emerging issues such as deductions relating to short-term rental properties to ensure they are genuinely available to rent.

Lowering tax and super liabilities

From

1 July 2023

The ATO and Treasury will be funded to address the growth in tax and superannuation liabilities. The focus is on:

High-value debts over $100,000

Aged debts older than two years where those taxpayers are either:

Public and multinational groups with an aggregated turnover of greater than $10 million, or

Privately owned groups or individuals controlling over $5 million of net wealth.

Small business lodgment penalty amnesty

Small businesses with an aggregated turnover of less than $10m, will be able to access a lodgment penalty amnesty program. The amnesty will remit failure-to-lodge penalties for outstanding tax statements lodged in the period from 1 June 2023 to 31 December 2023 that were originally due during the period from 1 December 2019 to 29 February 2022.

GST compliance program extended

From

1 July 2023

The ATO will receive over $588m over 4 years to continue its work to improve GST compliance. The funding is also intended to help the ATO develop more sophisticated analytical tools to combat emerging risks.

The measure is estimated to increase receipts by $7.6bn and increase payments by $3.8bn over the 5 years from 2022-23.

Serious Financial Crime Taskforce and Serious Organised Crime program extended and merged

From

1 July 2023

The Government will extend funding for the Serious Financial Crime Taskforce (SFCT) and Serious Organised Crime program (SOC) over 4 years to 30 June 2027 and merge the programs, with a merged SFCT to commence from 1 July 2023.

Anti-slavery Commissioner

An Anti-Slavery Commissioner will be established to work across Government, industry and society, to support compliance with the Modern Slavery Act 2018, improving transparency of supply chains.

Other

Support for SMEs and start-ups

An Industry Growth Program will support SMEs and start-ups to commercialise their ideas and grow their operations (businesses operating in the National Reconstruction Fund are a priority). The program has $392.4 million over 4 years.

An additional $39.6m over 4 years will support the Single Business Service to help SMEs engage with Government.

A small business wardens program through the Council of Small Business Organisations Australia (COSBOA) will support small businesses to build in-house capability to protect against cyber threats. $23.4 million has been provided over 3 years from 2023-24.

Disruptive defence technology funding

$3.4bn over 10 years has been provided to the Department of Defence to establish the ‘Advanced Strategic Capabilities Accelerator.’ Working with Australian industry, the accelerator seeks to “to lift capacity to translate disruptive new technologies into Defence capability rapidly.” Hmmm.

Direct pathway for kiwis to become Australian citizens

The Government will provide a direct pathway to Australian citizenship for New Zealand citizens in Australia from 1 July 2023, by allowing those who hold a non-protected Special Category visa (subclass 444), and meet general residence and other eligibility requirements, to apply directly for citizenship without becoming permanent residents first.

Reintroduction of work hour cap on international student visa holders

From

1 July 2023

During the pandemic, the cap on the number of hours an international student visa holder could work was removed.

From 1 July 2023 a work cap of 48 hours per fortnight will be reinstated. International students working in the aged care sector will be exempt from the cap until 21 December 2023.

International student post-study work rights extended